Russia produced only around 2,600 tonnes of rare earth oxide in both 2017 and 2018, about 2% of global output, despite having the world’s fourth largest reserves of the group of 17 metals with unique electronic and magnetic properties which are vital to most modern electronic products.

China’s virtual monopoly on the supply of the metals, which comprise the 15 lanthanides, scandium and yttrium, slid into focus once more at the end of May as trade tensions with the U.S. boiled over, yet again raising the profile of alternative sources. China produced 120,000 tonnes of rare earth oxide in 2018, accounting for around 70% of the world total, while the U.S. has just one operating mine, the [almost ironically] Chinese-owned Mountain Pass operation in California, which produced 15,000 tonnes in the same period. Australia took second place with output of 20,000 tonnes per annum.

China aside, the distribution of reserves tells a different story. Russia ranks fourth with approximately 12 million tonnes, dwarfing top producers Australia (3.4 Mt) and the U.S. (1.4 Mt), according to U.S. Geological Survey data; though President Vladimir Putin has claimed the country ranks second since it estimates reserves differently, or even probably first given its vast, underexplored territory.

Russia, however, faces a host of problems in developing deposits and production. First and foremost is the issue of processing technology. “Making sure that the refining technology is right for the mine is more critical in the rare earth space than it is in other mining sectors, so just the astronomical amounts [of material] it takes to produce small amounts of rare earths, and the risks, make developing rare earth facilities more fraught than copper or iron ore,” David Abraham, a senior fellow at think tank New America, told S&P Global Market Intelligence.

“The problems also concern development; a number of promising fields are located in Eastern Siberia in difficult climatic conditions, which in the current level of maturity of development technologies leads to high capital intensity of projects,” Deloitte CIS’ head of research projects, Dmitry Kasatkin, told S&P Global MI.

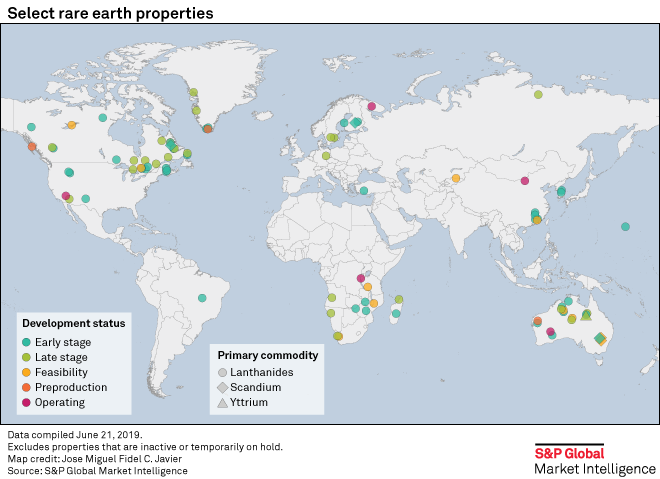

Nevertheless, Russia has a number of projects at different stages of development. Tomtorskoye in the north of the Sakha Republic and the Zashikhinskoye deposit in Irkutsk Oblast are the most promising in terms of potential completion, George Voloshin, who runs the Paris office of consultancy Aperio Intelligence, told S&P Global MI.

State-owned technology conglomerate Rostec Corp. struck a US$1 billion deal in 2013 to develop Tomtorskoye in a venture with Polymetal International PLC-founder Alexander Nesis’s ICT Group, but progress has been slow and long-term financing is still uncertain. Further delays are likely given the degree of technical complexity involved, according to Voloshin. The project is being run through TriArk Mining LLC, which hopes to produce 16,000 tonnes of rare earth oxide per annum from the deposit, as well as 14,000 tonnes of ferroniobium, an alloy used in high-strength low-alloy steel.

Developing Tomtorskoye is the only way to sharply increase Russia’s extraction of rare earths and production of collective concentrates, the Ministry of Industry and Trade told S&P Global MI, also highlighting Zashikhinskoye as among “several large-scale projects” launched to date, despite being conspicuously absent from the Ministry of Natural Resources latest report on Russia’s mineral resource base.

State Support

The advent of rare earths has by no means gone unnoticed by Moscow, which is trying to develop the industry through a support program that started in 2013 and is running until 2020. It aims to reduce Russia’s dependence on imports by establishing a guaranteed supply of rare earth-bearing concentrates but also to overcome the trickier challenge of extracting the metals domestically. The results of the program have, so far, been fragmented, with most of the implemented measures relating to research and development, according to Kasatkin. Russia currently imports 90% of the processed rare earths it consumes, mostly from China, according to Voloshin.

Putin himself in 2016 described the metals as critical to Russia’s defense capability, modern weapons and military equipment; though their largest use is in permanent magnets, a key component of electric vehicles. Russia’s domestic consumption is currently weak at just over 1,000 tonnes per annum, 80% of which takes place within the petrochemical sector, according to Kasatkin.

Russia’s State Duma [lower house] passed a draft law lowering the tax rate on rare earth extraction from 8% to 4.8% in February, which still has to go through a review process before being signed into law by Putin. “Despite this new focus on a capital-intensive and technologically complex industry, Russia doesn’t seem to be especially well-positioned at the moment to profit from its significant reserves,” Voloshin said. Work is also underway on a draft strategy for the industry’s development until 2035.

Despite their collective name, most rare earths are quite prevalent, but extracting and processing them is technologically complex, and Russia lags behind China and the U.S. in this respect. The Kremlin allocated 4.2 billion rubles to research and development over four years in 2013, and 40 R&D initiatives were completed by the end of 2016. Nevertheless, Russia exports 95% of the rare earth concentrate it currently produces due to its lack of separation plants, the Ministry of Industry and Trade told S&P Global MI.

Fertilizer producers and rare earths

Potash producer PJSC Acron began developing a process to extract rare earths from the apatite at its Oleniy Ruchey phosphate mine in 2010 with state support. The US$50 million plant in Veliky Novgorod was inaugurated by Putin in 2016, and produces cerium, lanthanum and neodymium. It is the only industrial-scale project in Russia separating rare earth concentrates into individual metals, but also produces concentrates of light and medium-heavy rare earths. It has an annual capacity of 200 tonnes of rare earth oxide, according to the Ministry of Industry and Trade. Commercial output of 100% oxides totaled 87.2 tonnes in 2018, according to Acron’s annual report.

At the start of June, another fertilizer-maker, JSC Uralchem, signed an agreement with state officials and Moscow-based SkyGrad Innovations to produce rare earth concentrates from waste dumps of phosphogypsum, a faintly radioactive byproduct of processing apatite. SkyGrad plans to set up a processing plant near Uralchem dumps on the outskirts of the city of Voskresensk, southeast of Moscow, with an initial annual capacity of around 100,000 tonnes. This could rise to as much as 700,000 tonnes, according to the agreement signed at the Saint Petersburg International Economic Forum. The first stage is planned for completion in 2020 and the second between 2022 and 2025 at an overall cost of 98 million rubles, with financing currently under negotiation.

Meanwhile, the lion’s share of Russia’s ore production comes from just one source, the Lovozerskoye deposit in Murmansk Oblast, operated by LLC Lovozersky GOK. Likewise, one company, OJSC Solikamsk Magnesium Works in Perm, accounts for almost 100% of Russia’s output of rare earth compounds, according to its website. Solikamsk, known as SMW, processes Lovozerskoye’s loparite ore, which contains light earths such as lanthanum, cerium and praseodymium, and produces carbonates and oxides of rare earths, from which individual metals can be eventually extracted. The company shipped 2,500 tonnes in 2017, according to its annual report for the same year [the most recent available], most of which went to Europe (71.2%) and Asia (28.5%). SMW’s output is further processed at TSX-listed Neo Performance Materials Inc.’s Silmet plant in Estonia.

CEO Vitaly Nesis of Russia’s gold and silver producer Polymetal International said in June that the company is very keen to invest in rare earths, with a focus on developing technology. He said the true upside in the sector would come not from the trade tensions between Beijing and Washington, but the nascent electric vehicle market.

Trade tensions

Asked whether Russia could profit from trade tensions between the U.S. and China, the Ministry of Industry and Trade said that “after creating separation plants on an industrial scale, the primary task will be to provide the Russian market with domestically produced individual REM oxides, and in the future the export of individual REM oxides is possible.” Production from Tomtorskoye would “significantly” increase the export component, the ministry added, concluding, “Russian companies will act in accordance with the market conditions that will emerge as a result of China restricting its export of rare-earth metals.”

“Russia is clearly far behind the dominant producer, China, and the global tech leader, the U.S., whose consumption of REM is strategically more important, if not vital, than Russia’s,” Voloshin said of trade tensions between the two countries. “The implementation of REM projects requires considerable long-term financial commitments, and first results will become apparent only 6-7 years later in a best-case scenario,” he noted.

The rare earth sector is certain to develop in Russia, particularly if the state is supportive, according to Kasatkin. However, in order to achieve a certain level of maturity, that is to control at least 10% of the world market, Russia will require time and favorable external conditions, such as low geopolitical and economic risks, he said. “Our experts talk about the possibility of such a development only over a 15 year horizon.”

“The trade war between China and the US may well have accelerated China’s drive to source rare earth and other critical minerals in ‘friendlier’ jurisdictions,” Jack Lifton, a senior fellow at the Institute for the Analysis of Global Security, told S&P Global MI. “China does not foresee a problem selling growing amounts of rare earth enabled products into its domestic economy nor to foreign customers. The issue today is Chinese concern for their declining reserves of critical rare earths. Thus China is favorably disposed to financing Russian projects such as … Tomtor[skoye], … which would be closer to Beijing than to Moscow. Tomtor would have, as a byproduct, substantial quantities of the magnet rare earths. China could also benefit from increased rare earth production at Lovozero [Lovozerskoye].”

“I suspect that Chinese geologists are already cooperating with the Russians looking for rare earth deposits,” Lifton added.