A recent report by IDTechEx states that the lithium-ion battery market will reach over $430 billion by 2033.

According to the analyst, electric cars and transportation will represent the largest market.

“Battery electric cars will constitute over 90% of Li-ion demand, by GWh, by 2033,” the report reads. “This will be driven by the increasing adoption of electric vehicles with more stringent emissions targets and goals and as EVs begin to reach cost parity with conventional ICE vehicles.”

IDTechEx’s experts also see significant market opportunities in consumer electronics, electronic devices, and stationary energy storage systems.

“Given the rapid pace of growth, significant investment has been placed on increasing production capacities for Li-ion batteries,” the report states.

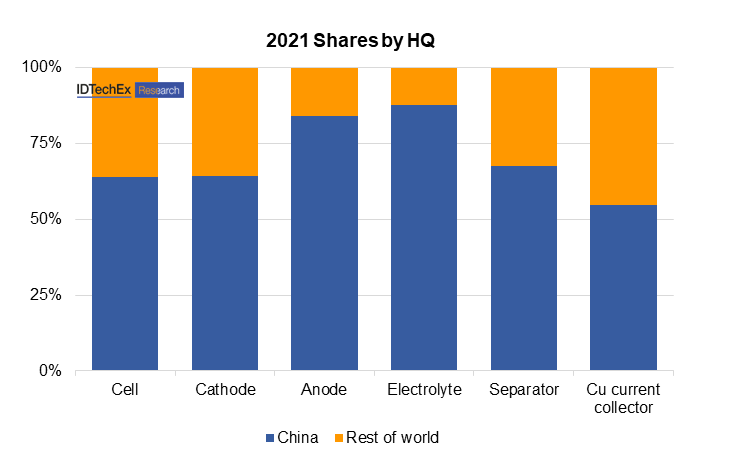

“While a significant number of announcements and plans are in place for the development of battery supply chains in Europe and North America, China currently dominates.”

IDTechEx estimates that 70% of Li-ion cells were produced in China in 2021, and though this share is likely to shift to Europe and USA over the next five years, China is still expected to hold over 50% of manufacturing capacity by 2028.

The research firm notes that a large domestic market for both electric vehicles and stationary storage, and a strategic outlook on the importance of the battery market, have helped foster China’s strong position.

Raw materials

Looking at the impact of raw material prices on Li-ion battery adoption, IDTechEx notes that the upward trend has continued despite considerable headwinds over the past year, particularly connected to lithium and nickel substantial price increases.

The analyst’s data show that such increases have led to the adoption of lower-cost battery technologies such as lithium iron phosphate, which has seen a resurgence in China and is gaining popularity in Europe and the US among automakers, as well as in the stationary storage sector.

“However, a shift to LFP would further consolidate China’s leading position with the vast majority of LFP cathode and batteries produced in China,” IDTechEx warns. “Options, including high-manganese cathodes, high voltage LNMO, and silicon-based anodes, are being explored and commercialized in efforts to not only improve performance but reduce costs and supply chain risks.”