Electric vehicle sales keep growing, and quite fast. Year over year, gas car sales have been going down and electric car sales have been going up. The transition is underway. But there are periods of faster growth and periods of slower growth. When growth is slower than expected, that can lead to an oversupply of batteries and an oversupply of EV battery materials. The prices of those then drop, which decreases the price of EVs, which accelerates growth.

When growth is faster than expected, that can lead to a crunch in the battery supply chain. That’s what McKinsey & Company is forecasting will happen by 2030. “Fast-increasing demand for battery raw materials and imbalanced regional supply and demand are challenging battery and automotive producers’ efforts to reduce Scope 3 emissions,” the consultancy firm writes.

McKinsey & Company thinks global sales of passenger electric vehicles will go from 4.5 million in 2021 to 28 million in 2030, a more than sixfold increase. If we want that growth to be faster, or to sustain through 2030, the battery material supply chain needs to keep up. Otherwise, limited supplies will raise prices and slow growth. “For producers of battery cells and raw materials, ensuring a reliable and ample supply of sustainable and affordable materials will be crucial to their competitiveness, the ongoing rollout of BEVs, and the net-zero transition overall.” On the latter front, EVs are expected to help with grid storage and grid stability as wind and solar power become a bigger and bigger portion of the electricity pie.

The analysis notes that slower than expected EV growth in 2024 has led to a financial crunch on battery and battery material companies, which also dampens investments into future production capacity.

McKinsey & Company also notes that the goal through all of this — scaling up of battery supply chains while remaining fiscally solvent — we also want battery material extraction and processing to be as green — as environmentally sensitive — as possible. “However, to meet net-zero transition goals, companies that produce and consume battery materials will need to balance the three dimensions of the “materials trilemma”4 by ensuring availability (meeting growing demand needs and ensuring regional security of supply), affordability (maintaining competitive prices to ensure affordability of materials and the products and applications that are built from those materials), and sustainability (complying with or exceeding the environmental, social, and governance (ESG) standards and requirements set out by governments, customers, and industry associations alike) of materials.” Indeed.

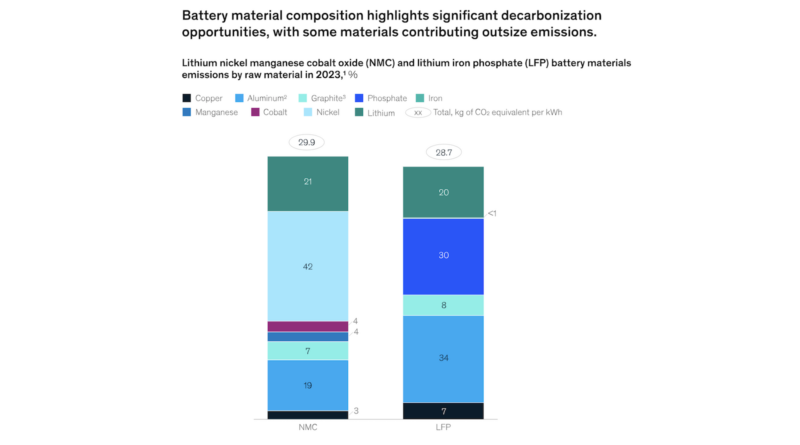

It’s extra hard balancing all of these things when you add in another wildcard — which battery chemistries will be used? Or, more precisely, what proportion of EV batteries will be LFP, what proportion will be NMC, what proportion will be new sodium-based batteries, etc., etc.? If 70% of EV batteries are going to be LFP batteries in 2030, that’s a dramatically different supply chain than if 30% will be.

McKinsey & Company then goes into a pretty thorough examination of different EV battery materials and different scenarios for the future for them. You can check out the full analysis here. Check it out and let us know if any big points jump out at you — positively or negatively.