A recent, 200-page report released by Australia’s science agency CSIRO indicates that the national electricity market (NEM) could require a 10 to 14-fold increase in its electricity storage capacity between 2025-2050. This, in order to respond to rapidly rising energy demand spurred by the ongoing electrification of building and transport industries.

The study also found that while traditional storage technologies, such as batteries and pumped hydro, will continue to play a key role, all forms of energy storage must be considered to meet Australia’s growing demand across multiple sectors, each of which may favour different storage technologies.

“Although there are existing storage systems used to deliver energy from fossil fuels, higher levels of renewables in Australia’s energy system will result in a greater requirement for renewable energy storage technologies. These include electricity storage through electrochemical processes (e.g. batteries), mechanical storage (e.g. pumped hydro energy storage [PHES]), chemical storage (e.g. hydrogen in tanks or pipelines) and thermal storage (e.g. molten salts),” the report reads.

According to the document, batteries may be the best option for local and short-duration storage of electricity while thermal or heat energy – like steam – might be technology better suited for heat-intensive industries.

The roadmap uses a scenario-based approach, building on pathways developed in the Australian Energy Market Operator’s 2022 Integrated System Plan that could materially impact the country’s energy sector.

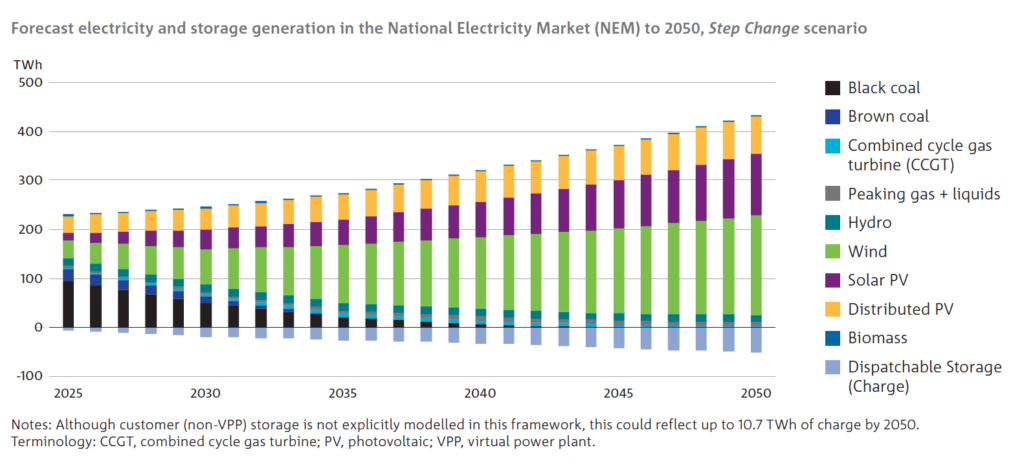

In two of the cases, the Step Change and Hydrogen Superpower scenarios, the suggestion is that the national electricity market could require 44–96 GW/550–950 GWh of dispatchable electricity storage capacity by 2050, with Western Australia alone requiring 12–17 GW/74–96 GWh.

“As Australia transitions to net zero, there may also be an increase in thermal storage requirements, driven by the greater need for renewable process heat in industrial production,” the dossier states. “In addition, the strong profile for hydrogen exports in the Hydrogen Superpower scenario will lead to large increases in the demand for both electricity and hydrogen storage systems.”

Large investments

Despite the uncertainty in storage outcomes in 2050, the modelling results suggest that all net-zero pathways will require large investments in renewable energy storage capacity.

In particular, larger investments in short- and medium-duration electricity storage are expected to be required to provide a reliable electricity supply, and significant investments in hydrogen (or hydrogen carrier) storage systems would be required if Australia wants to become a leader in green hydrogen exports.

Local mining tycoon Andrew Forrest has been at the forefront of the green hydrogen revolution, building and expanding facilities to manufacture electrolyzers, as the demand outlook for the clean fuel strengthens.

In CSIRO’s view, investment is also likely to be required for thermal energy storage systems, given the important role of process heat in industry and the use of variable renewable energy for heat production and the requirement for a constant heat supply.

“Determining the most competitive and appropriate forms of energy storage requires an understanding of the context in which the storage system will be used,” the agency’s document reads. “This requires stakeholders to go through a site- and region-specific approach to understand the role of energy storage, the deployment considerations and the technology options available (both commercial and developing). This approach is critical because site and regional factors can affect the requirements, costs, risks and integration considerations for a given storage system.”

Not an easy road

CSIRO’s report notes that, regardless of the positive trend toward renewable energy deployment, many Australian sectors face challenges in integrating storage technologies.

When it comes to short-duration electricity storage (1–4 hours), which is expected to play a major role in decarbonization across Australia’s grids and industries, particularly by 2030, supply chain risks could create deployment bottlenecks and drive up prices.

To address this issue, CSIRO’s experts recommend the development of strategies to de-risk battery supply chains through a number of strategic diversification pathways, including, but not limited to strategic supply chain and manufacturing partnerships; developing domestic value chains; developing resource circularity; and investing in research, development and demonstration for alternative battery chemistries.

Looking at medium (4–12 hours) and long intraday (12–24 hours) electricity storage, the report recognized that although some commercial technologies exist, they are not always applicable depending on the end use or region in question. There are also several other technology options currently in development, but these are not yet competitive and require further demonstration and deployment.

Thus, the suggestion is to rapidly demonstrate and commercially deploy medium to long intraday duration technologies capable of providing hundreds of megawatt hours to multiple gigawatt hours of storage to create a diverse set of options for major grids and industry applications.

The dossier also proposes the idea of conducting further regional studies to better understand geological storage opportunities, such as with adiabatic compressed air energy storage and PHES subsystems, and opportunities to take advantage of existing capital and sites, including evaluating opportunities created through mine closure efforts.

In the case of long multiday (24–48 hours) and seasonal (100+ hours) electricity storage, which is expected to play a key energy ‘insurance’ and resilience role in major and isolated grids, the main issue is that storage technology options are limited and often have long lead times, with many stakeholders still considering investment options, including those that minimize storage investments, and evaluating trade-offs as they transition to net zero.

Given this situation, CSIRO believes that it is crucial to conduct further analysis to better understand Australia’s requirements for multiday and seasonal storage, the trade-offs that exist and the technology pathways available.

“Develop the pipeline of projects to meet Australia’s potential long-term seasonal and multi-day needs, including identifying and implementing opportunities to accelerate PHES deployments, and progressing emerging multi-day and seasonal technologies,” the report recommends.

The roadmap also proposes feasible pathways when it comes to the storage needed for mid‑temperature processes (150–500°C), high‑temperature processes (500°C and above) and hydrogen and hydrogen carriers.