ADEME, France’s Environment and Energy Management Agency, carried out a study with IFP Energies nouvelles (IFPEN) on the dynamics of lithium supply and demand, based on different scenarios for the electrification of the global car fleet by 2050.

The lithium market continues to grow; in 2015, the market grew by 5% a year, and supply will have to increase sharply to meet future demand.

According to the scenarios developed in this study, a high penetration of electric vehicles worldwide (up to 75% of the stock of vehicles in 2050) would not entail a geological supply risk, as reserves are sufficient in the long run.

On the other hand, this could lead to a marked decrease in the safety margin of lithium supply—the ratio between the cumulative consumption and current reserves—and a possible significant volatility of lithium prices by 2050.

More generally, vulnerabilities economic, industrial, geopolitical or environmental issues are still possible.

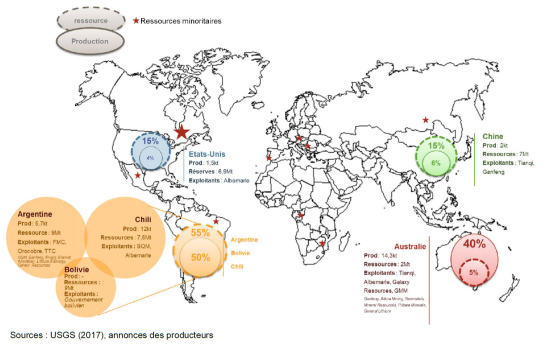

Production is currently concentrated between Australia (40%), Argentina and Chile (50% between them). The latter two countries belong to the lithium triangle (Argentina, Bolivia and Chile), which represents about 55% of the world’s resources. The strategies of these 3 countries will have a decisive weight in the medium- and long-term capacity to supply lithium to industrial players, especially in Europe.

Further, vulnerabilities could emerge from increased competition among lithium buyers. China, which has put in place a policy of security of supply, will have competitive advantages and will be able to favor its internal market to the detriment of the importing countries. Developments in China’s trade policy will therefore become an essential parameter of the market, according to the report.